Surprising Tips for Managing Student Loan Debt After Graduation in 2025.

Although graduating from college is a significant accomplishment, student loan debt is frequently a significant financial burden. Few graduates are completely equipped to handle the realities of managing such payments immediately after graduation, even if many anticipate paying off their loans over time.

The good news? You may prevent needless worry and stay ahead of your loans with several little-known but incredibly powerful techniques.

We’ll go over some unexpected advice and clever strategies in this article to help you manage your student loan debt so you can concentrate on developing your future and profession rather than becoming bogged down in payments.

Get a financial professional today

Surprising Tips for Managing Student Loan Debt After Graduation in 2025

It can be difficult to make the move from college to the workforce, particularly when student loans are due. Maintaining financial stability and reaching professional objectives require knowing the terms of your loan and creating a clear payback plan. When repayment obligations start, it’s critical to expedite the procedure and look into strategies to lower interest rates and accelerate debt repayment.

Recognize When Payments Need to Start

When your enrollment status changes—for example, when you graduate, withdraw, or enroll less than half-time—you usually start repaying your federal student loans. There is a six-month grace period before payments are due for the majority of borrowers with Direct Subsidized or Unsubsidized Loans. Similar grace periods are provided by Perkins Loans, albeit each institution may have a different time frame.

While graduate borrowers automatically receive a six-month deferment, PLUS Loans taken out for undergraduate education do not have a grace period.

Examine Your Options for a Repayment Plan

There are two main types of repayment plans: income-based and fixed-payment.

Your monthly payment remains constant under fixed-payment plans:

- Standard Plan: Payback period of ten years. The duration of consolidated loans might range from 10 to 30 years.

- Graduated Plan: Usually over a ten-year period, lower beginning payments rise every two years.

- Extended Plan: Provides fixed or progressive repayment plans over a 25-year period.

Payments under income-driven repayment (IDR) are determined by family size and earnings. There are four main IDR plans available:

- Repayment Based on Income (IBR)

- Repayment of Income Contingent (ICR)

- PAYE, or pay as you earn,

- Preserving a Priceless Education (SAVE)

Your loans will default to the regular ten-year repayment schedule if you don’t choose a plan, or longer if you consolidate.

Effective Payment Management

The Department of Education contracts with loan servicing organizations to manage billing and repayment. They will walk you through your options and let you know when payback begins.

- Direct and FFEL Loans: Your servicer receives payments.

- Perkins Loans: The designated billing agency or the school receives payments.

Techniques for Quicker Repayment

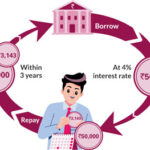

Many borrowers take about 20 years to pay back their debts, however you can cut that number down by a few years:

- Make additional payments: Principal and interest are decreased when monthly payments exceed the minimum.

- Make the switch to bi-weekly payments: Dividing your payment into two installments every two weeks results in 26 half-payments, which is the same as making one more monthly payment annually.

- Take out a loan refinance: Refinancing may reduce your interest rate if you have good credit and a consistent income, but be aware that federal protections like as income-based plans and forgiveness alternatives will no longer be available.

- Employ autopay: On federal loans, enrolling in automatic payments might result in an interest rate reduction, usually around 0.25%, which lowers monthly payments and interest expenses.

Private Loans Need to Be Handled Differently

Lenders like banks or credit unions oversee private student loans, in contrast to federal loans. These lenders determine their own conditions, such as interest rates, payback plans, and safeguards for borrowers. You must speak with the lender directly to discuss any relief or adjusted repayment terms because private loans are exempt from federal restrictions.

Although student loans are an effective way to pay for college, they can be difficult to return once you graduate. Take the time to comprehend your repayment plan, adjust it to your financial circumstances, and employ techniques to speed up payments to prevent feeling overburdened.

Contact your loan servicer right away if you run into problems. Effective loan debt management and the creation of a stable financial future are possible with forethought and prompt action.

In conclusion

After graduation, managing student loan debt doesn’t have to mean living paycheck to paycheck. You can achieve steady development without jeopardizing your financial security if you employ the appropriate tactics, some of which may surprise you. Being proactive can help you avoid frequent repayment traps, enroll in the appropriate repayment plan, and take advantage of employer support.

Being informed, taking prompt action, and routinely reviewing your repayment plan are crucial. You’ll take charge of your money and create the foundation for sustained success by doing this.